Your credit score: what is it and why it matters

What is a credit score?

A credit score is a three-digit number that represents your past borrowing and payment behavior. Although there are hundreds of different “credit scoring models” used by creditors and the credit reporting bureaus, the most recognized is the FICO® Score (although there are many versions of this model too). Because the FICO Score is the most recognized and often used, we will focus the remainder of this article on that scoring model.

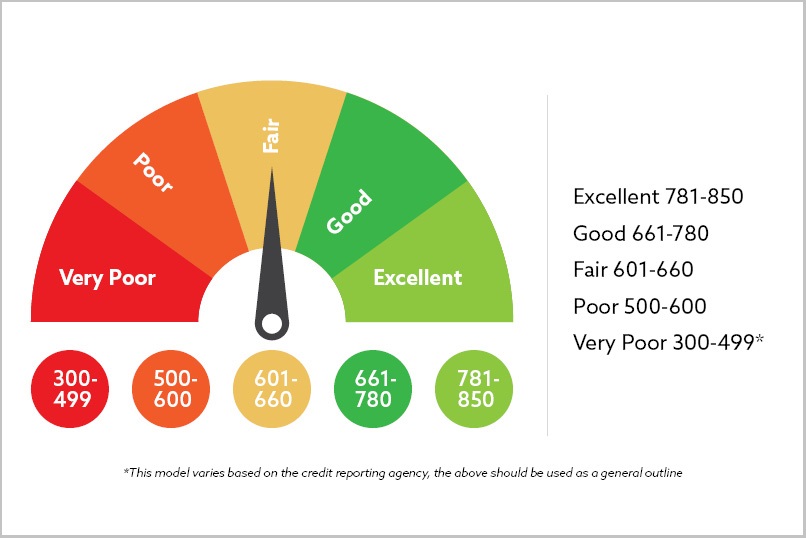

FICO Scores range between 300 to 850. Creditors use this number to determine your creditworthiness and how likely you are to pay money back. It is important to know, there are three primary credit reporting bureaus used by creditors– Experian, Equifax and Transunion—however, there are others. It’s normal for the credit scores provided by each credit bureau to differ from each other.

How is a credit score determined?

Credit reporting bureaus pay attention to five factors when calculating your credit score. However, the factors are not equally important; certain categories are weighted more heavily than others. Let’s talk about it:

- 35% Payment History – Payment history refers to whether and how often payments are late or missed. Typically, payments made over 30 days late will be reported by your lender and may negatively impact your credit score.

- 30% Amounts Owed – This is the amount of debt you have and the ratio of that amount to the amount of credit you have available to you. Note, 0% utilization may be viewed less favorably than some usage! Ideally, your usage should be around 30% or less of your available credit line.

- 15% Length of Credit History – The longest, shortest, and average amount of time your credit accounts have been open will be considered for this category. Generally, the longer your credit history – the better!

- 10% Credit Type - When assessing credit scores, lenders and credit bureaus like to see that you are able to maintain a mix of accounts. Having a variety of accounts, whether a home loan, auto loan, or credit cards - your credit score can improve.

- 10% New Credit – New credit activity, like applying for a new credit card, may help build your score. But keep in mind, if you open several accounts too quickly, it could counteract your efforts and lower your score.

Why does your credit score matter?

Your credit score may impact your financial options more than you realize. While your score will be pulled when you apply for loans like credit cards or home loans, it may also be checked when applying for things like renting a new apartment or setting up utilities in your name. Making sure you are aware of changes to your credit score and understanding how to build stronger credit will help set up for financial success.

Let’s review:

Start early. Make sure you are aware of your credit score and if you have questions, the Simmons Bank app offers a credit monitoring tool, powered by Experian to help you keep up with your Vantage 3.0 credit score. We recommend checking your score monthly for updates and ensuring all items on your report are accurately stated. Contact us today with any questions!

More articles from our Learning Center:

How to pay off debt

How to set savings goals

Simple ways to save

Tips to minimize check fraud

Easy tips to spot and avoid fraud